GB/T 39870-2021 PDF EnglishUS$255.00 · In stock · Download in 9 seconds

GB/T 39870-2021: Brand Valuation - Automobile Manufacturing Industry Delivery: 9 seconds. True-PDF full-copy in English & invoice will be downloaded + auto-delivered via email. See step-by-step procedure Status: Valid

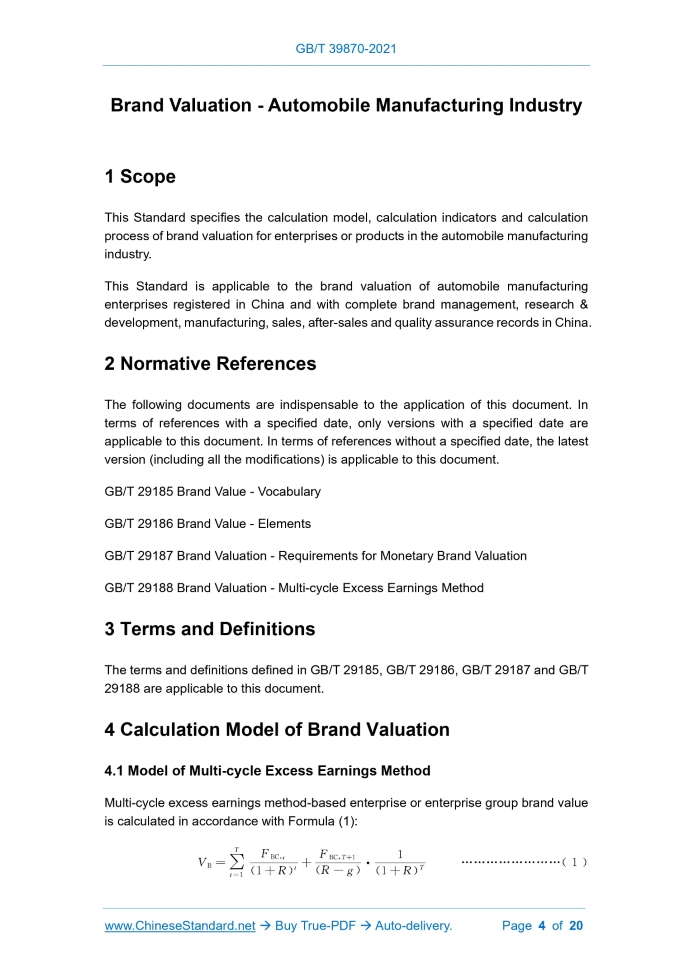

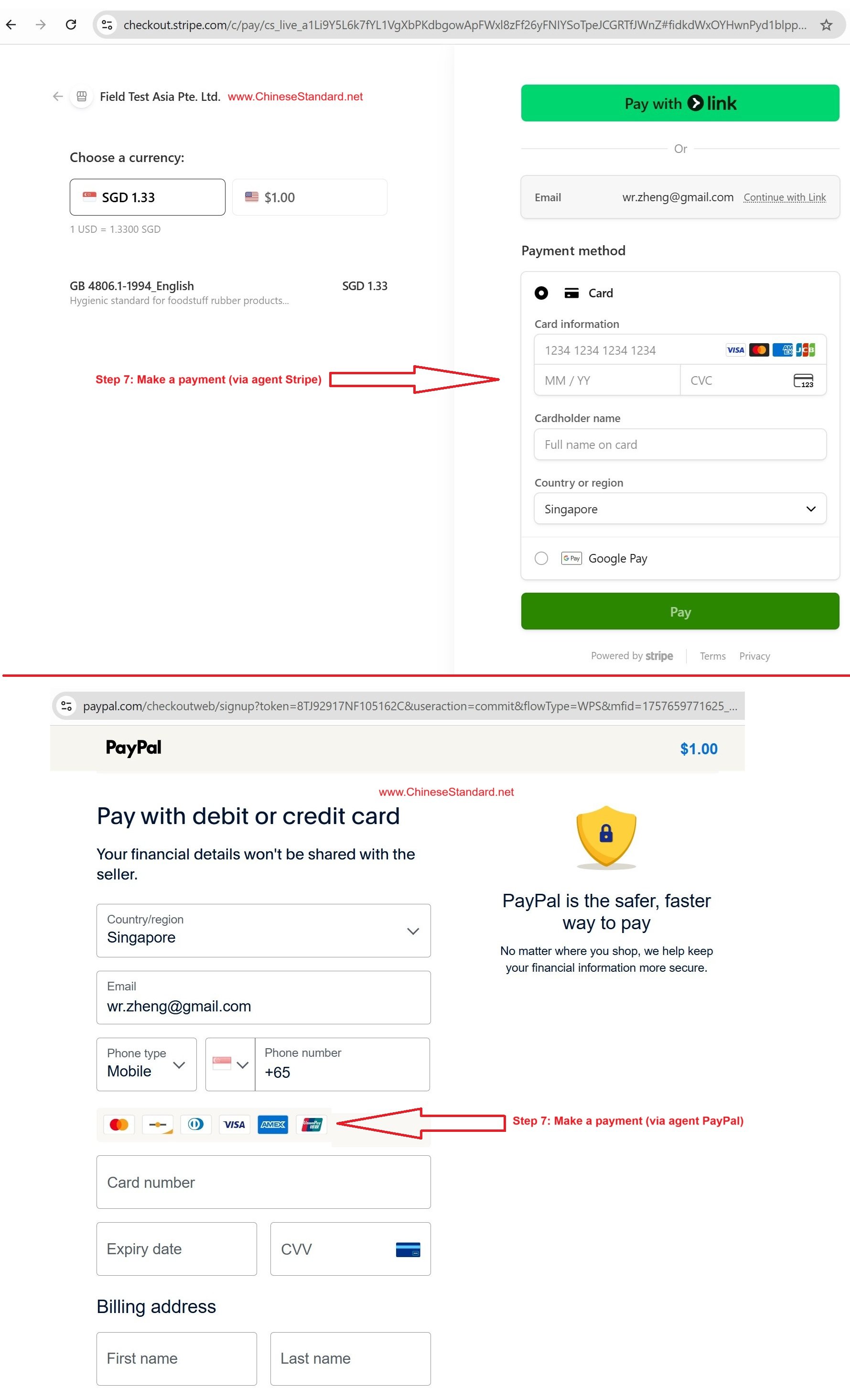

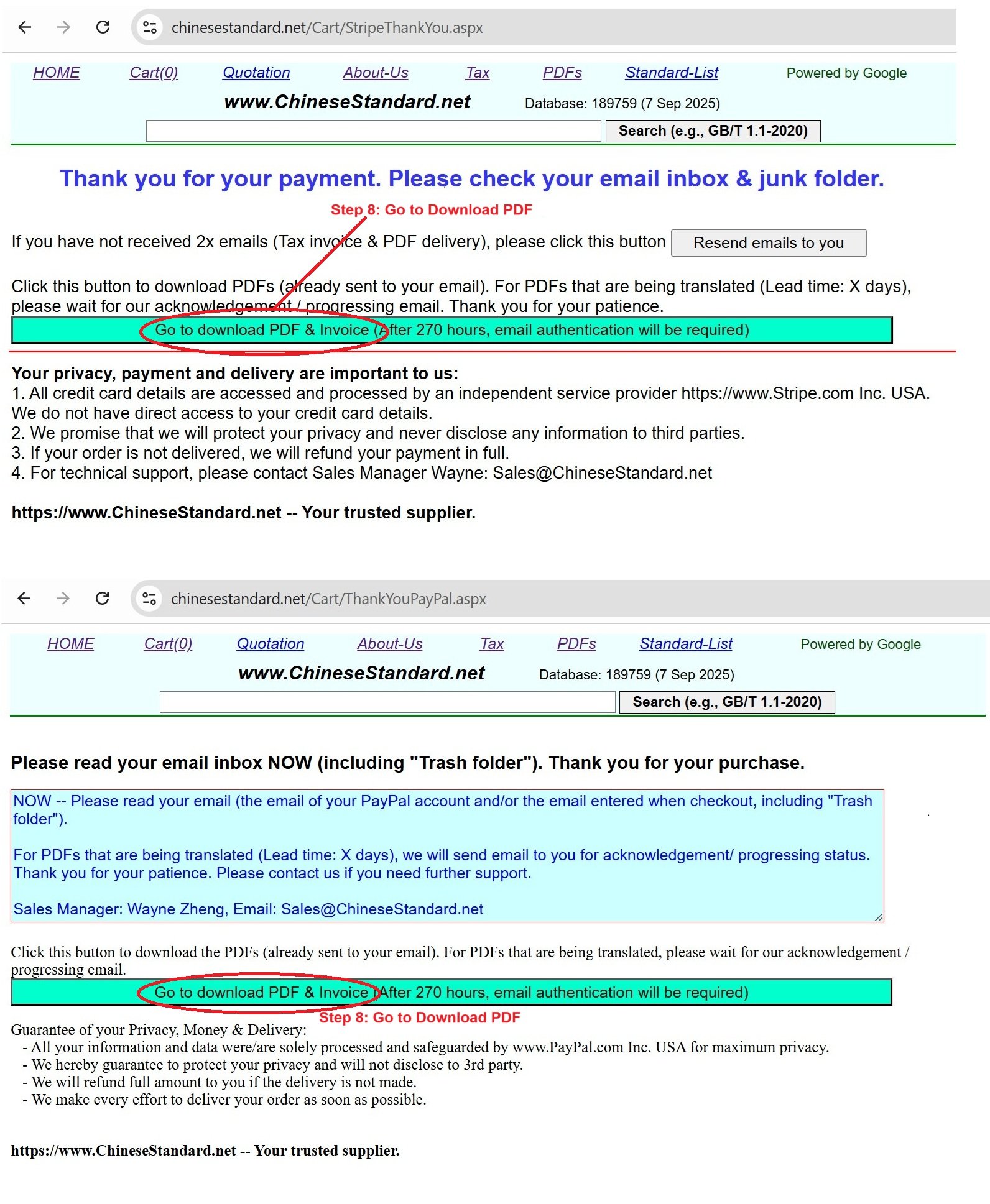

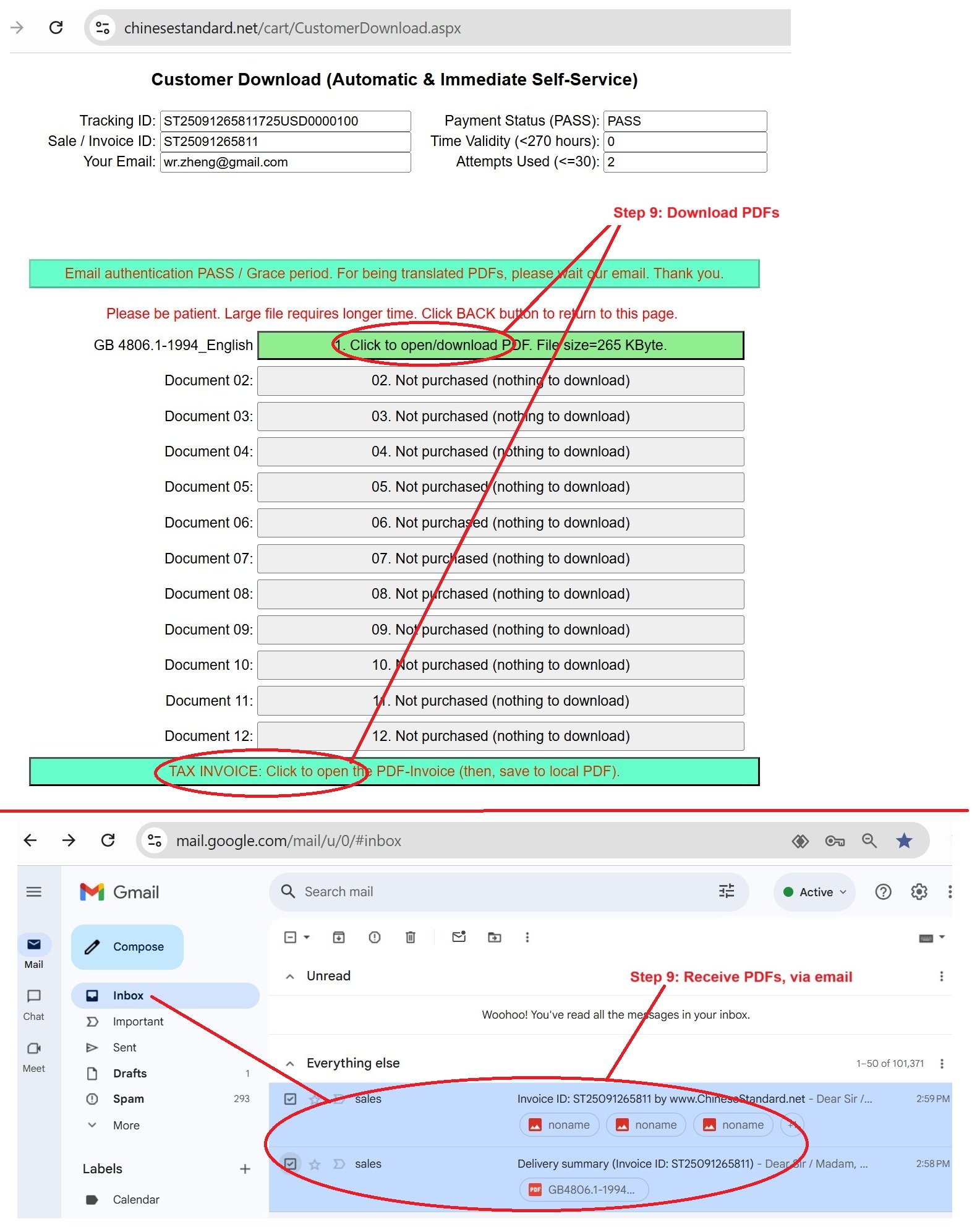

Similar standardsGB/T 39870-2021: Brand Valuation - Automobile Manufacturing Industry---This is an excerpt. Full copy of true-PDF in English version (including equations, symbols, images, flow-chart, tables, and figures etc.), auto-downloaded/delivered in 9 seconds, can be purchased online: https://www.ChineseStandard.net/PDF.aspx/GBT39870-2021GB NATIONAL STANDARD OF THE PEOPLE’S REPUBLIC OF CHINA ICS 03.140 A 00 Brand Valuation - Automobile Manufacturing Industry ISSUED ON: MARCH 9, 2021 IMPLEMENTED ON: OCTOBER 1, 2021 Issued by: State Administration for Market Regulation; Standardization Administration of the People’s Republic of China. Table of ContentsForeword ... 3 1 Scope ... 4 2 Normative References ... 4 3 Terms and Definitions ... 4 4 Calculation Model of Brand Valuation ... 4 4.1 Model of Multi-cycle Excess Earnings Method ... 4 4.2 Determination of Brand Cash Flow ... 5 4.3 Determination of Brand Value Discount Rate ... 6 5 Brand Strength Calculation Indicators ... 7 5.1 Overview ... 7 5.2 Tangible Element (K1) ... 8 5.3 Quality Element (K2) ... 8 5.4 Innovation Element (K3) ... 8 5.5 Service Element (K4) ... 9 5.6 Intangible Element (K5) ... 9 6 Brand Value Calculation Process ... 10 6.1 Clarify Value Influencing Factors ... 10 6.2 Describe Calculated Brand ... 10 6.3 Determine Model Parameters ... 10 6.4 Collect Calculation Data ... 11 6.5 Execute Calculation Process ... 11 6.6 Report Calculation Results ... 11 Appendix A (informative) Brand Strength Calculation Indicators and Descriptions of Automobile Manufacturing Industry ... 12 Bibliography ... 20 Brand Valuation - Automobile Manufacturing Industry1 ScopeThis Standard specifies the calculation model, calculation indicators and calculation process of brand valuation for enterprises or products in the automobile manufacturing industry. This Standard is applicable to the brand valuation of automobile manufacturing enterprises registered in China and with complete brand management, research & development, manufacturing, sales, after-sales and quality assurance records in China.2 Normative ReferencesThe following documents are indispensable to the application of this document. In terms of references with a specified date, only versions with a specified date are applicable to this document. In terms of references without a specified date, the latest version (including all the modifications) is applicable to this document. GB/T 29185 Brand Value - Vocabulary GB/T 29186 Brand Value - Elements GB/T 29187 Brand Valuation - Requirements for Monetary Brand Valuation GB/T 29188 Brand Valuation - Multi-cycle Excess Earnings Method3 Terms and DefinitionsThe terms and definitions defined in GB/T 29185, GB/T 29186, GB/T 29187 and GB/T 29188 are applicable to this document.4 Calculation Model of Brand Valuation4.1 Model of Multi-cycle Excess Earnings Method Multi-cycle excess earnings method-based enterprise or enterprise group brand value is calculated in accordance with Formula (1): Where, IA---the tangible assets income; ACT---the total amount of current tangible assets; CT---the rate of income on investment of current tangible assets; ANCT---the total amount of non-current tangible assets; NCT---the rate of income on investment of non-current tangible assets. 4.2.2.3 Return on current tangible assets The return on current tangible assets may be calculated with reference to the short- term benchmark loan interest rate issued by the People’s Bank of China, for example, the one-year bank loan benchmark interest rate. 4.2.2.4 Return on non-current tangible assets The return on non-current tangible assets may be calculated with reference to the long- term benchmark loan interest rate issued by the People’s Bank of China, for example, the five-year bank loan benchmark interest rate. 4.3 Determination of Brand Value Discount Rate 4.3.1 Brand value discount rate The brand value discount rate shall be calculated in accordance with Formula (4): Where, R---the brand value discount rate; Z---the industrial average rate of income on assets; k---the brand strength coefficient. 4.3.2 Industrial average rate of income on assets The industrial average rate of income on assets may be obtained by calculating the average rate of income on assets of listed enterprises in similar industries, types and scales. Or the industrial average rate of income on assets may also be obtained through the mode of statistical survey. 5.2 Tangible Element (K1) The tangible element may be evaluated through the perspective of market influence. Market influence includes but is not limited to: ---Domestic market; ---Overseas market; ---New energy vehicle market; ---Business conditions. 5.3 Quality Element (K2) 5.3.1 Quality management Quality management includes but is not limited to: ---Management system; ---Management performance. 5.3.2 Quality level Quality level includes but is not limited to: ---Product quality; ---Product quality supervision; ---Enterprise’s energy conservation and environmental protection; ---Enterprise safety. 5.3.3 Quality reputation Quality reputation includes but is not limited to: ---Quality credit; ---Quality honor. 5.4 Innovation Element (K3) 5.4.1 Innovation achievements Innovation achievements include but are not limited to: ---New model sales; ---Brand honor; ---Brand loyalty; ---Brand awareness; ---Brand culture; ---Brand building system; ---Brand equity. 5.6.2 Social responsibility Social responsibility includes but is not limited to: ---Management mechanism; ---Public responsibility; ---Employee care; ---Social activity. 5.6.3 Compliance management Compliance management includes but is not limited to enterprise compliance.6 Brand Value Calculation Process6.1 Clarify Value Influencing Factors The tangible, quality, innovation, service and intangible elements of an enterprise shall be comprehensively considered, especially the influence of non-financial factors, such as: quality and innovation, on brand value. 6.2 Describe Calculated Brand Before calculation, the brand under evaluation shall be identified, defined and described, including its product range and value range, etc. 6.3 Determine Model Parameters In accordance with relevant national policies and regulations, and the current market economy, determine: ---The year and cycle of evaluation; ......Source: Above contents are excerpted from the full-copy PDF -- translated/reviewed by: www.ChineseStandard.net / Wayne Zheng et al. Tips & Frequently Asked Questions:Question 1: How long will the true-PDF of English version of GB/T 39870-2021 be delivered?Answer: The full copy PDF of English version of GB/T 39870-2021 can be downloaded in 9 seconds, and it will also be emailed to you in 9 seconds (double mechanisms to ensure the delivery reliably), with PDF-invoice.Question 2: Can I share the purchased PDF of GB/T 39870-2021_English with my colleagues?Answer: Yes. The purchased PDF of GB/T 39870-2021_English will be deemed to be sold to your employer/organization who actually paid for it, including your colleagues and your employer's intranet.Question 3: Does the price include tax/VAT?Answer: Yes. Our tax invoice, downloaded/delivered in 9 seconds, includes all tax/VAT and complies with 100+ countries' tax regulations (tax exempted in 100+ countries) -- See Avoidance of Double Taxation Agreements (DTAs): List of DTAs signed between Singapore and 100+ countriesQuestion 4: Do you accept my currency other than USD?Answer: Yes. www.ChineseStandard.us -- GB/T 39870-2021 -- Click this link and select your country/currency to pay, the exact amount in your currency will be printed on the invoice. Full PDF will also be downloaded/emailed in 9 seconds.How to buy and download a true PDF of English version of GB/T 39870-2021?A step-by-step guide to download PDF of GB/T 39870-2021_EnglishStep 1: Visit website https://www.ChineseStandard.net (Pay in USD), or https://www.ChineseStandard.us (Pay in any currencies such as Euro, KRW, JPY, AUD).Step 2: Search keyword "GB/T 39870-2021". Step 3: Click "Add to Cart". If multiple PDFs are required, repeat steps 2 and 3 to add up to 12 PDFs to cart. Step 4: Select payment option (Via payment agents Stripe or PayPal). Step 5: Customize Tax Invoice -- Fill up your email etc. Step 6: Click "Checkout". Step 7: Make payment by credit card, PayPal, Google Pay etc. After the payment is completed and in 9 seconds, you will receive 2 emails attached with the purchased PDFs and PDF-invoice, respectively. Step 8: Optional -- Go to download PDF. Step 9: Optional -- Click Open/Download PDF to download PDFs and invoice. See screenshots for above steps: Steps 1~3 Steps 4~6 Step 7 Step 8 Step 9 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}