GB/T 31047-2023 PDF EnglishUS$245.00 · In stock · Download in 9 seconds

GB/T 31047-2023: Brand valuation - Food processing and manufacturing industry Delivery: 9 seconds. True-PDF full-copy in English & invoice will be downloaded + auto-delivered via email. See step-by-step procedure Status: Valid GB/T 31047: Historical versions

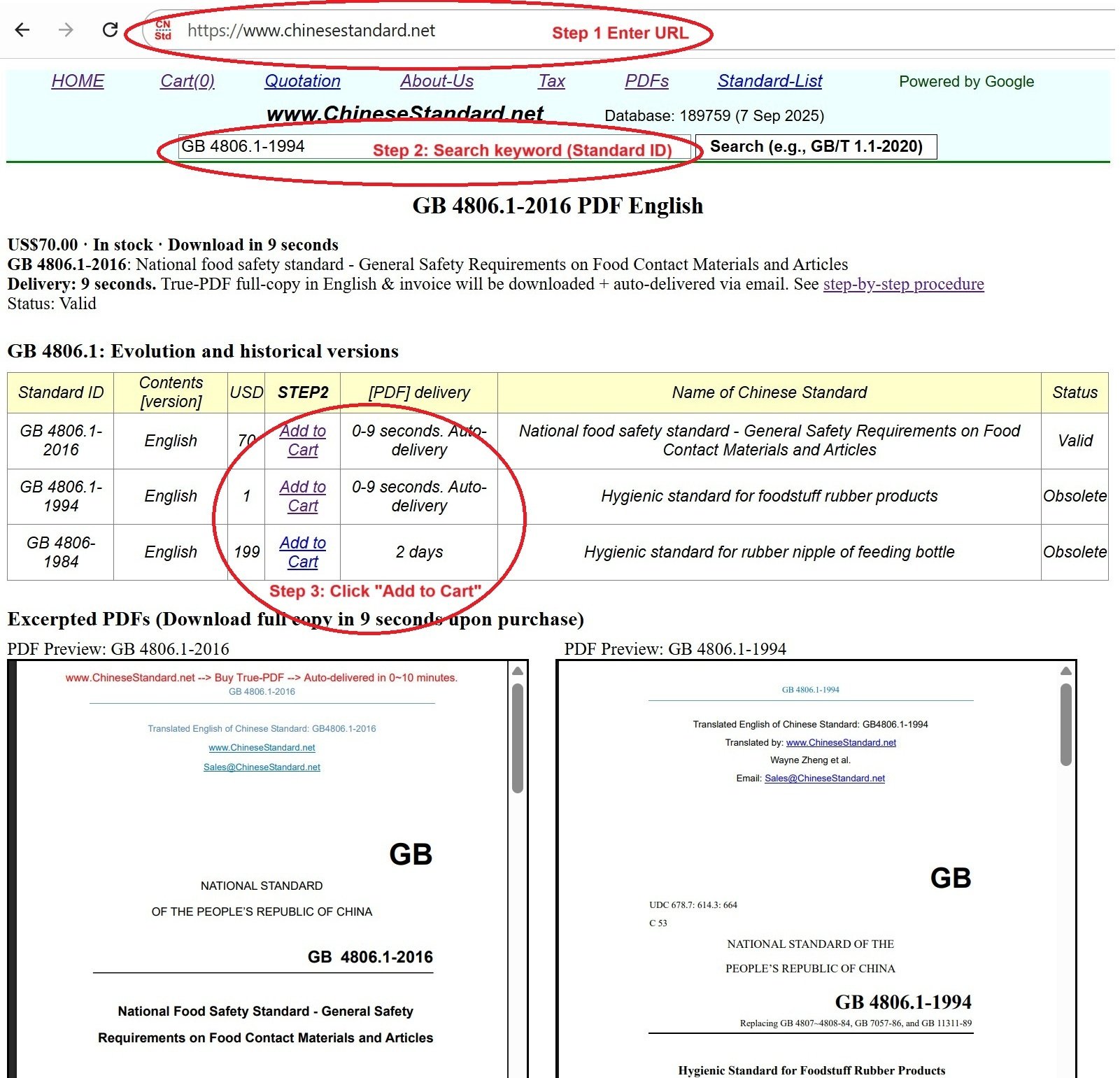

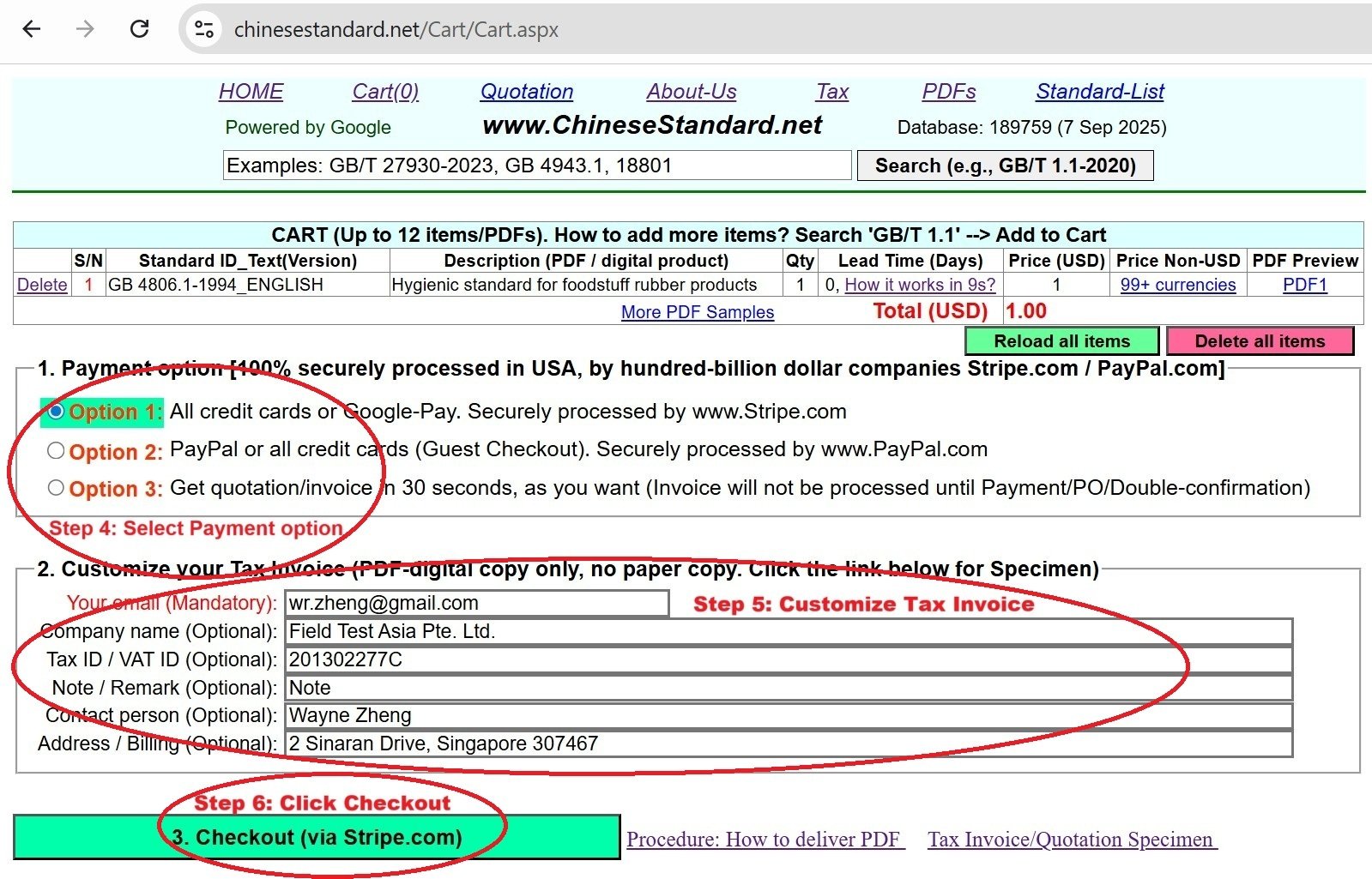

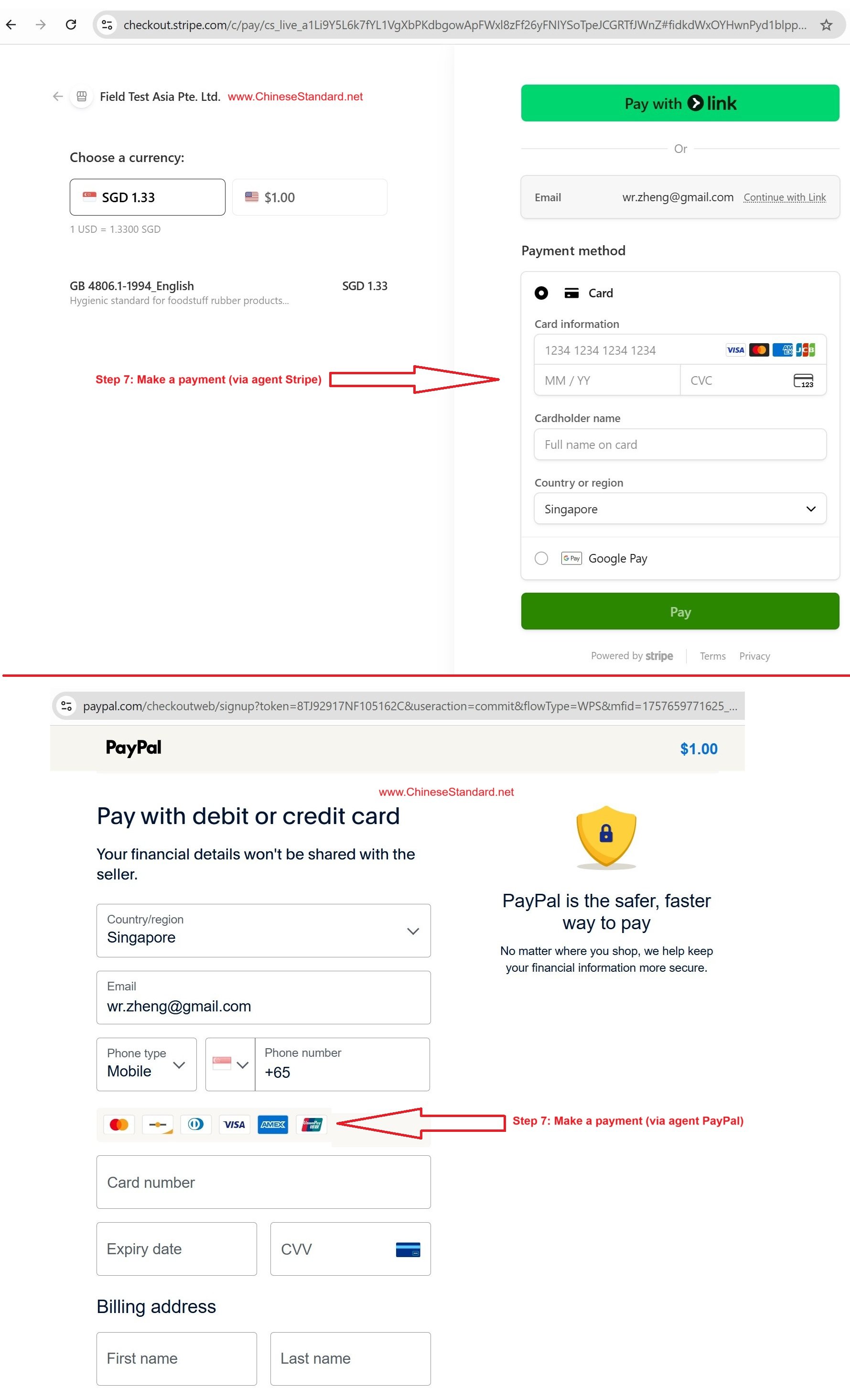

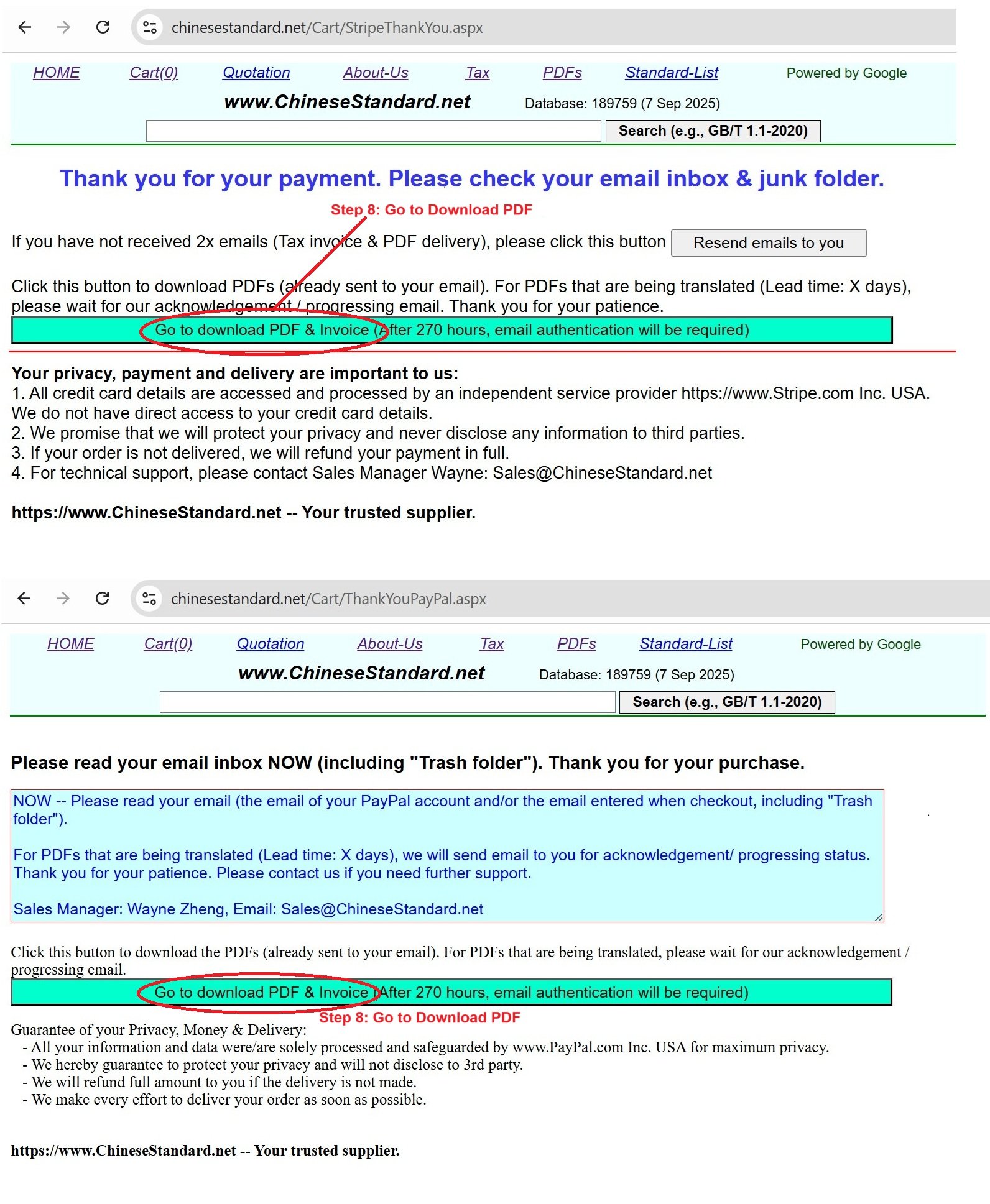

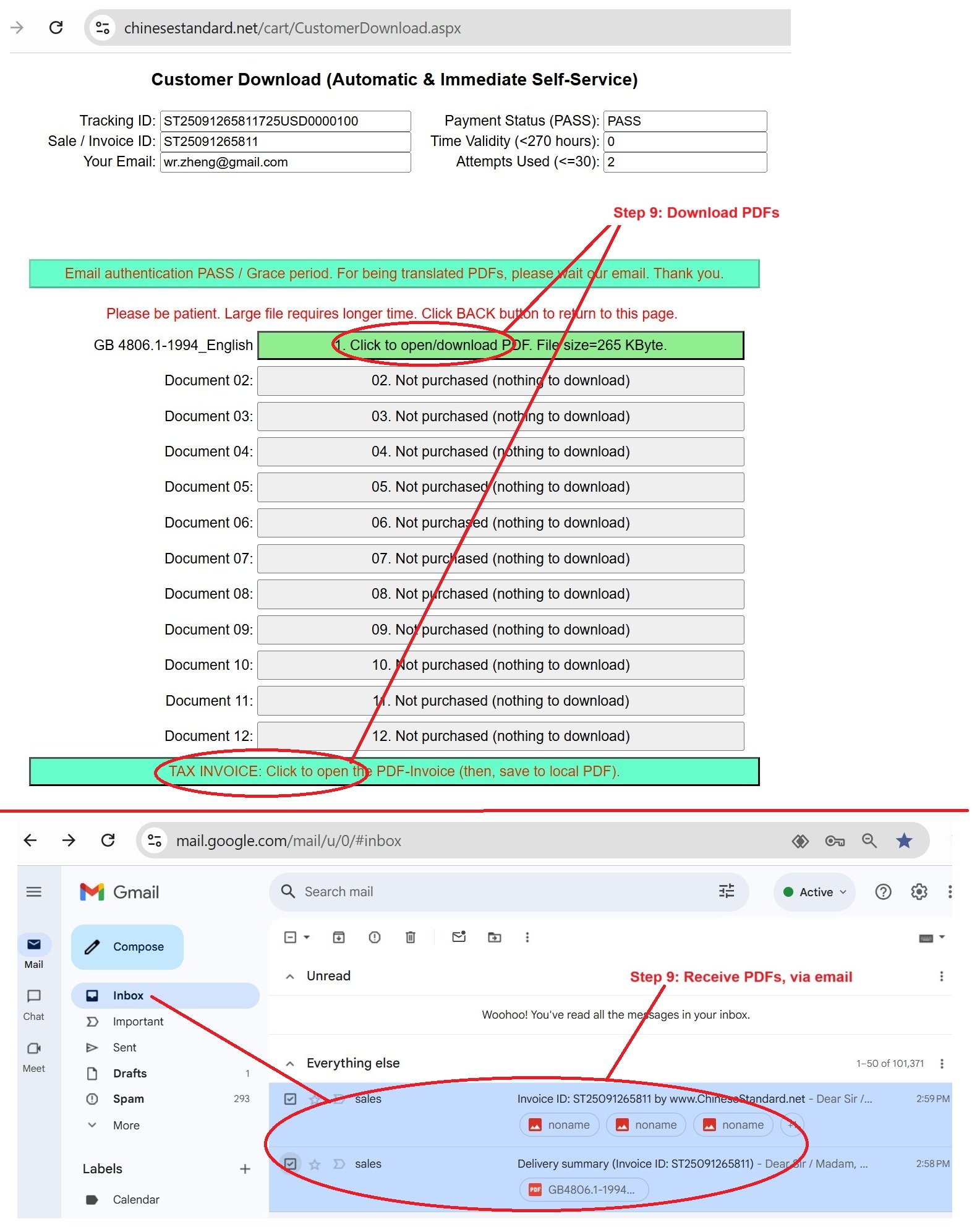

Similar standardsGB/T 31047-2023: Brand valuation - Food processing and manufacturing industry---This is an excerpt. Full copy of true-PDF in English version (including equations, symbols, images, flow-chart, tables, and figures etc.), auto-downloaded/delivered in 9 seconds, can be purchased online: https://www.ChineseStandard.net/PDF.aspx/GBT31047-2023GB NATIONAL STANDARD OF THE PEOPLE’S REPUBLIC OF CHINA ICS 03.140 CCS A 00 Replacing GB/T 31047-2014 Brand Valuation - Food Processing and Manufacturing Industry ISSUED ON: MARCH 17, 2023 IMPLEMENTED ON: MARCH 17, 2023 Issued by: State Administration for Market Regulation; Standardization Administration of the People’s Republic of China. Table of ContentsForeword ... 3 1 Scope ... 4 2 Normative References ... 4 3 Terms and Definitions ... 4 4 Brand Strength ... 5 5 Evaluation Model ... 7 6 Evaluation Process ... 9 Appendix A (informative) Brand Strength Indexes and Descriptions ... 12 Appendix B (informative) Optional Evaluation Methods ... 14 Bibliography ... 16 Brand Valuation - Food Processing and Manufacturing Industry1 ScopeThis document provides the brand strength, evaluation model and evaluation process of brand valuation in the food processing and manufacturing industry. This document is applicable to the enterprises and products in the food processing and manufacturing industry in carrying out brand valuation. This document is not applicable to the evaluation of regional brands.2 Normative ReferencesThe contents of the following documents constitute indispensable clauses of this document through the normative references in the text. In terms of references with a specified date, only versions with a specified date are applicable to this document. In terms of references without a specified date, the latest version (including all the modifications) is applicable to this document. GB/T 29185 Brand - Vocabulary GB/T 29186 (all parts) Evaluation of Brand Value Elements GB/T 29187 Brand Valuation - Requirements for Monetary Brand Valuation GB/T 29188 Brand Valuation - Multi-cycle Excess Earnings Method3 Terms and DefinitionsWhat is defined in GB/T 29185, GB/T 29186 (all parts), GB/T 29187 and GB/T 29188, and the following terms and definitions are applicable to this document. 3.1 food processing Food processing refers to various operations that change the shape, size, nature or purity of raw materials of food or semi-finished products, so that they can conform to the food standards. [source: GB/T 15091-1994, 2.3] 3.2 food manufacturing Food manufacturing refers to the entire process of processing raw materials of food or semi- finished products into substances that can be eaten or drunk by human beings. [source: GB/T 15091-1994, 2.2]4 Brand Strength4.1 Overview The forecasting and calculation indexes of brand strength of the food processing and manufacturing industry include: tangible element (K1), quality element (K2), innovation element (K3), service element (K4) and intangible element (K5). See Appendix A for the evaluation indexes and contents at all levels. 4.2 Tangible Element The evaluation indexes can include: ---market leadership; ---market development capability; ---profitability. 4.3 Quality Element The evaluation indexes can include: ---product quality and food safety level; ---product quality and food safety management level; ---food quality and food safety credit status. 4.4 Innovation Element The evaluation indexes can include: ---innovation capability; ---innovative achievements. 4.5 Service Element The evaluation indexes can include: ---service capability; ---customer relations. Different evaluation objectives will affect the evaluation procedures, evaluation accuracy and the form of results reporting. 6.2 Determine Evaluation Object and Scope Before the evaluation, the evaluation object shall be identified, defined and described, including the scope of its products or services, and the scope of brand valuation, etc. 6.3 Judge the Applicability of Evaluation Method In accordance with the characteristics of the brand being evaluated, judge the applicability of the evaluation method. When selecting an evaluation method, the following factors may be considered, but not limited to: a) Evaluation objective; b) Brand management status, for example, profitability; c) Availability of the data of various evaluation indexes involved in the method; d) Consistency requirements for evaluation results. 6.4 Determine Model Parameters In accordance with the relevant monetary policies and industry development policies of the country, region and industry where the brand is located, the economic conditions of the current market and the selected evaluation method, determine the following model parameters: a) Year and cycle of evaluation; b) Earnings forecasting method; c) Perpetual growth rate within the evaluation cycle; d) Industry average return on assets; e) Proportionality factor for the portion of the intangible asset income attributable to the brand. 6.5 Collect Evaluation Data Follow the principles of authenticity, accuracy and objectivity, collect all kinds of data needed for evaluation. The channels for obtaining evaluation data include, but are not limited to: ---Information and data publicly released or provided by the brand being evaluated;Appendix B(informative) Optional Evaluation Methods B.1 Cost Approach The cost approach is an evaluation approach of forecasting and calculating the brand value by deducting the depreciation caused by various losses on the basis of the replacement cost of brand building. When adopting this approach, the brand being evaluated should satisfy, but not limited to the following conditions: ---The brand being evaluated can continue to be used, that is, it can bring prospective earnings to its owner; ---There are cost information on brand establishment and maintenance, etc. B.2 Market Approach The market approach forecasts and calculates the value of the brand being evaluated by comparing the similarities and differences between the brand being evaluated and the comparable brand, and adjusting the evaluation value of the comparable brand. When adopting this approach, the brand being evaluated should satisfy, but not limited to the following conditions: ---The existence of comparable brands similar to the brand being evaluated; ---Be able to collect and obtain market information, financial information and other relevant materials of the comparable brands; ---For the comparable brands, multiple brands in the same industry are generally chosen for comparison, and the most reasonable and appropriate brands are selected from them. NOTE: there are few relevant cases of brands being traded as independent assets. In addition, even if data of the comparable objects is available, the characteristics of the brand being evaluated may be significantly different from those of the few brands being traded. B.3 Incremental Cash Flow Method The incremental cash flow method identifies the cash flow generated when the enterprise uses the brand compared to when the brand is not used. When adopting this method, the brand being evaluated should satisfy, but not limited to the following conditions: ---The cost-saving cash flow generated compared to when the brand is not used by the subject of evaluation; ......Source: Above contents are excerpted from the full-copy PDF -- translated/reviewed by: www.ChineseStandard.net / Wayne Zheng et al. Tips & Frequently Asked Questions:Question 1: How long will the true-PDF of English version of GB/T 31047-2023 be delivered?Answer: The full copy PDF of English version of GB/T 31047-2023 can be downloaded in 9 seconds, and it will also be emailed to you in 9 seconds (double mechanisms to ensure the delivery reliably), with PDF-invoice.Question 2: Can I share the purchased PDF of GB/T 31047-2023_English with my colleagues?Answer: Yes. The purchased PDF of GB/T 31047-2023_English will be deemed to be sold to your employer/organization who actually paid for it, including your colleagues and your employer's intranet.Question 3: Does the price include tax/VAT?Answer: Yes. Our tax invoice, downloaded/delivered in 9 seconds, includes all tax/VAT and complies with 100+ countries' tax regulations (tax exempted in 100+ countries) -- See Avoidance of Double Taxation Agreements (DTAs): List of DTAs signed between Singapore and 100+ countriesQuestion 4: Do you accept my currency other than USD?Answer: Yes. www.ChineseStandard.us -- GB/T 31047-2023 -- Click this link and select your country/currency to pay, the exact amount in your currency will be printed on the invoice. Full PDF will also be downloaded/emailed in 9 seconds.Question 5: Should I purchase the latest version GB/T 31047-2023?Answer: Yes. Unless special scenarios such as technical constraints or academic study, you should always prioritize to purchase the latest version GB/T 31047-2023 even if the enforcement date is in future. Complying with the latest version means that, by default, it also complies with all the earlier versions, technically.How to buy and download a true PDF of English version of GB/T 31047-2023?A step-by-step guide to download PDF of GB/T 31047-2023_EnglishStep 1: Visit website https://www.ChineseStandard.net (Pay in USD), or https://www.ChineseStandard.us (Pay in any currencies such as Euro, KRW, JPY, AUD).Step 2: Search keyword "GB/T 31047-2023". Step 3: Click "Add to Cart". If multiple PDFs are required, repeat steps 2 and 3 to add up to 12 PDFs to cart. Step 4: Select payment option (Via payment agents Stripe or PayPal). Step 5: Customize Tax Invoice -- Fill up your email etc. Step 6: Click "Checkout". Step 7: Make payment by credit card, PayPal, Google Pay etc. After the payment is completed and in 9 seconds, you will receive 2 emails attached with the purchased PDFs and PDF-invoice, respectively. Step 8: Optional -- Go to download PDF. Step 9: Optional -- Click Open/Download PDF to download PDFs and invoice. See screenshots for above steps: Steps 1~3 Steps 4~6 Step 7 Step 8 Step 9 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}